Bankruptcy and Tax Refund Season - When is the best time to file bankruptcy if you are expecting a large tax refund?

Adrian Lynn • December 21, 2025

Is there a better time to file Bankruptcy based solely on tax refunds?

Why January Can be a Strategic Time to File Bankruptcy

For many people who get large refunds, January creates a unique opportunity:

1. Last Year’s Refund Is Usually Already Gone

By January:

The prior year’s refund has often been spent on living expenses, catching up bills, or holiday costs.

It’s no longer sitting in the bank creating exemption issues.

That can mean:

✔️ lower cash balances

✔️ fewer assets to protect

✔️ a cleaner financial snapshot at filing

For many clients in Fort Myers, Cape Coral, and Lehigh Acres, Naples and Florida this alone makes January an ideal time to move forward.

2. The New Refund Hasn’t Had Time to Build Up Yet

Even though refunds feel like something that happens in February or March, legally they start accruing on January 1 — with every paycheck.

If you wait until:

March, April, or later,

you may have already “earned” a significant portion of the upcoming refund, which could become part of the case and the trustee could take next year.

Filing earlier in the year often means:

✔️ less of the new refund is at risk

✔️ more flexibility in planning

3. Bank Account Balances Are Often Lower After the Holidays

Right after Christmas:

accounts are usually drained,

credit cards are maxed,

and refunds haven’t arrived yet.

In Florida, where cash in the bank can be an issue beyond limited exemptions, January often means:

✔️ fewer problems with bank balances

✔️ less stress over “what’s in the account” on filing day

4. January Can Help With the Chapter 7 Means Test

The Chapter 7 means test looks at your last six full months of income before filing.

For example:

Filing in January looks at income from July–December.

Filing in February looks at August–January.

For many people:

overtime, bonuses, or seasonal income happened earlier in the year,

while fall and winter income may be lower.

That means filing early can sometimes:

✔️ improve eligibility for Chapter 7

✔️ avoid being pushed into a Chapter 13 unnecessarily

This is a key reason early-year consults matter for clients throughout Fort Myers, Cape Coral, Naples and all of Florida.

Expecting a Big Refund for 2025? Planning Early Is Critical

If you know you typically receive a large refund for the current tax year, waiting until after it hits can limit your options.

When you talk to a bankruptcy lawyer in January or February, it allows time to:

plan around refund timing,

avoid panic spending,

consider adjusting withholding when appropriate, (this is a big deal if you usually use your tax refund as a savings account)

and choose the filing date that protects you best.

The earlier you get advice, the more tools your attorney has to work with to help you save and keep your refund.

Why “Waiting for the Refund to Fix It” Usually Backfires

We hear this every season:

“Once my refund comes, I’ll catch up.”

But in reality:

interest keeps growing,

late fees keep stacking,

emergencies pop up,

and minimum payments barely touch the balance.

A few months later, the refund is gone… and the debt is still there.

Worse, people sometimes use refunds to:

❌ pay one creditor (which can create problems before filing),

❌ drain accounts out of fear,

❌ or delay until lawsuits or garnishments start.

By then, what could have been strategic planning turns into damage control.

Bankruptcy Isn’t About Giving Up... It’s About Creating a Plan

For many families, bankruptcy can:

✔️ stop collection calls and lawsuits

✔️ halt foreclosures and repossessions

✔️ protect income and accounts

✔️ create breathing room

✔️ and offer a real path forward

The goal isn’t to erase responsibility — it’s to stop the constant emergency long enough to build something stable again.

The Big Takeaway: January Is About Options & Fresh Starts!

January isn’t “magic.” But for people expecting large tax refunds, it often offers:

✔️ last year’s refund already spent

✔️ new refund not yet built up

✔️ lower bank balances

✔️ favorable income lookback

✔️ more time to plan

In short: more control.

And when it comes to bankruptcy, timing can be everything.

Talk to a Florida Bankruptcy Attorney Before Your Refund Hits

If you live in Fort Myers, Naples, Cape Coral, Lehigh Acres, Bonita Springs, Estero, or anywhere in Florida and expect a tax refund this year, now is the time to get real answers.

At Lynn Law Group, we help individuals and families understand:

how tax refunds are treated in bankruptcy,

when to file,

and how to protect as much as the law allows and as their individualized situation requires.

Every situation is different — and a short conversation early in the year can make a life-changing difference!

📞 If you are ready for your fresh start, call us today for a free consultation and find out what your options really are.

This article is for informational purposes only and does not constitute legal advice. Reading this does not create an attorney-client relationship.

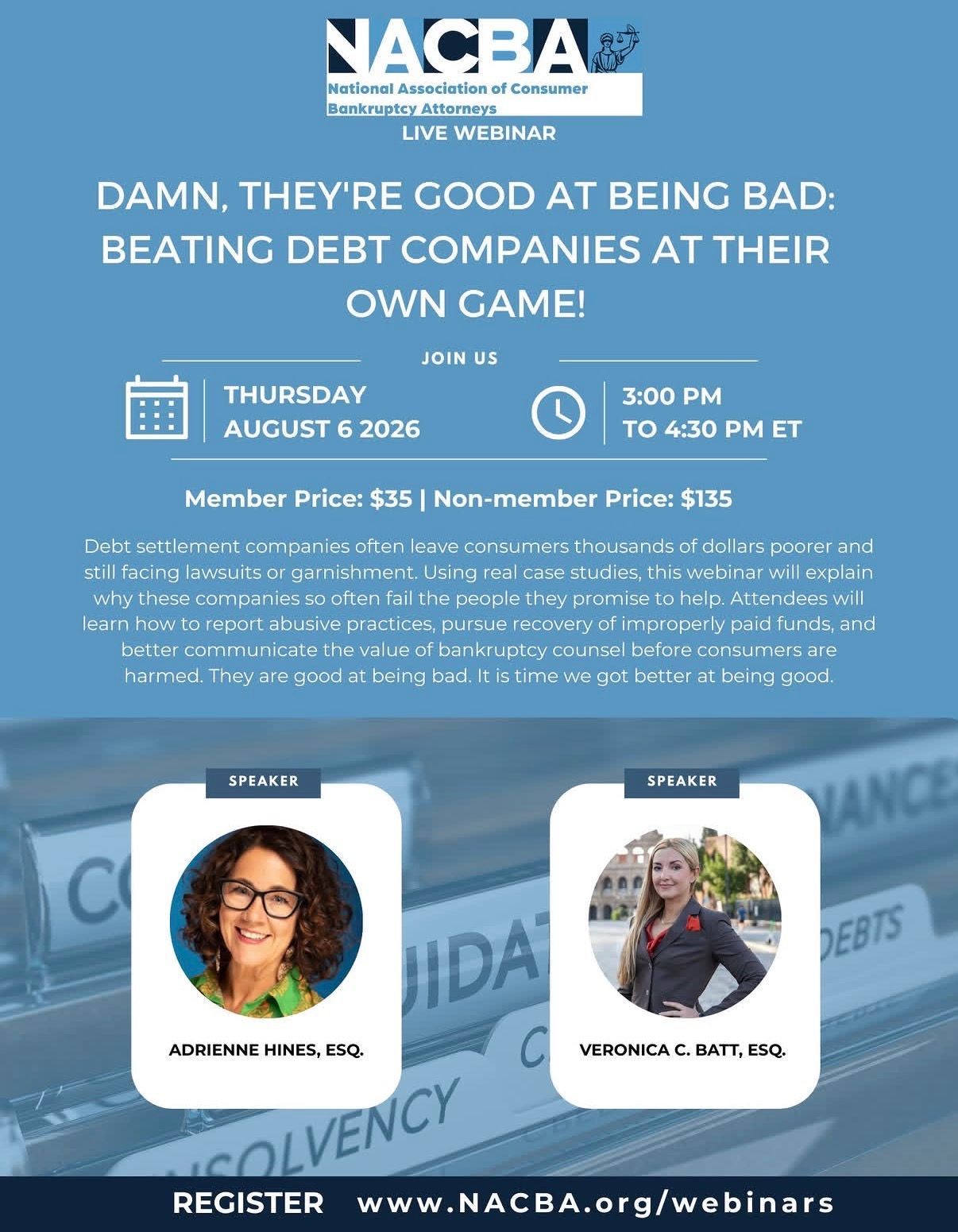

What I think bankruptcy attorneys need to know about debt settlement companies... and why protecting financially distressed consumers has become one of the most important conversations in consumer law.

I made a video recently mentioning that I've completed more than 60 hours of continuing legal education since October, almost all of it focused on bankruptcy and debt-related issues. For context, Florida attorneys are generally required to complete 30 hours of continuing legal education every three years to maintain their license. I've completed more than twice that amount in less than a year and all in bankruptcy related fields. The reason isn't because I'm trying to collect certificates or check boxes somewhere. The reason is simple: we take competence *very* seriously. When someone hires a bankruptcy lawyer, they are trusting that lawyer to guide them through a process that can have long-term consequences for their finances, their home, their business, and their future. That's not something we take lightly. Since October, Adrian and I have attended local and national bankruptcy programs, including NACBA conferences, consumer bankruptcy seminars, local ABI conferences, and most recently the Southern District of Florida Bankruptcy Workshop. At that workshop, we had the opportunity to hear directly from the full panel of bankruptcy judges serving in the Southern District of Florida and some trustees, about procedures, common issues, and developments affecting bankruptcy cases. What I find interesting is that after more than 25 years of practice and thousands of bankruptcy cases, Adrian is still sitting in those rooms learning too. That's how I think it should be. The law changes. Procedures change. Case law changes. Trustee practices change. If you're not constantly learning, you're falling behind. I don't believe continuing education should be something lawyers do every few years because they have to. I think it should be part of being a professional. At our office, we spend a significant amount of time learning because we want to make sure we're giving clients the most accurate and up-to-date advice possible. Sometimes that knowledge helps identify an exemption issue that saves a client money. Sometimes it's a strategy that helps someone keep a home. Sometimes it's knowing about a recent procedural change before it becomes a problem in a case. The point is that details matter. Bankruptcy law is incredibly technical, and there is always something new to learn. We're not doing this because we have to. We're doing it because our clients deserve attorneys who are committed to staying at the top of their game.

What We Brought Back From the NACBA Annual Conference in Boston We just got back from the National Association of Consumer Bankruptcy Attorneys Annual Conference in Boston, and it’s one of my fav trips of the year! Not just because of what we learned, but because of the conversations, the people, and the perspective it gives you on where things are heading. The AI Conversation No One Can Ignore One of the most important topics discussed this year was the use of AI in legal matters and bankruptcy specifically of course. And not in a vague, futuristic way. In a very real, happening-now way. There are cases starting to come out where courts are taking a closer look at how AI is being used by parties in litigation. That includes the potential for trustees or opposing parties to subpoena AI prompt and response histories. Think about that for a second.... If someone is typing questions into a free AI tool about their finances, their assets, or how to handle a legal situation, how to shield things from creditors, there may be little to no expectation of privacy. Unlike speaking with an attorney, there’s no privilege attached to those conversations. And if something becomes relevant in a case, it could potentially be discoverable. That’s a major shift. We’re also seeing, over and over again, that AI gets things wrong. Not just small details, but entire legal concepts. It fills in gaps with confidence, even when the information isn’t accurate. In our world, that can create real problems. I am starting to see quintessential ChatGPT outlines from clients and they are *dead* wrong. AI is eager to please you and will try (even hallucinating!) to give you the answer it thinks you want. We’ve had people come to us with plans they thought were “smart” because they read them somewhere or got them from an AI tool, only to find out those decisions could actually hurt their case. The takeaway here isn’t that technology is bad. It’s that there’s a difference between information and advice. And when it comes to your financial future, your home, your assets, your family… this is not something you want to get wrong. AI may get there someday, but that day is not today. The Energy of Being Around People Who Care About This Work Beyond legal updates, one of the best parts of the conference was being around other bankruptcy attorneys who genuinely care about what they do. This is a very specific area of law. The people who choose to do this work do it because they believe in it and those who stay in it, do it because they love it! They believe in giving people a way out, in protecting families, in helping someone reset and move forward. And when you get a group of those people in one place, the conversations are different. We talked through real scenarios. We compared approaches. We shared what’s working, what isn’t, and where things are heading. There’s a level of honesty in those conversations that you just don’t get anywhere else. It’s not competitive. It’s collaborative. The collaborative relationships help our clients too. Because every time we have one of those conversations, every time we hear how another attorney is handling a situation, it gives us more perspective. More tools. More ways to approach a case thoughtfully and strategically. That’s something we bring back with us. Why I think this is important for our clients... We don’t go to conferences just to say we went, or because we need more legal education credits (we already have tons!). We go because the law changes. The strategies evolve. Approaches change. And the stakes are too high to stay in one place. Our clients are trusting us with some of the most stressful moments of their lives. They deserve an attorney who is paying attention, who is learning, and who is constantly refining how they approach these cases. That’s what this kind of experience allows us to do. A Little Bit of Boston, Too Of Course! And in between everything, we managed to sneak in a little time to enjoy the city. We got a rare date night, which doesn’t happen often, and made our way to Mike's Pastry in the North End. If you’ve been, you already know… the cannoli are not small, the calories were not counted that night haha. At all. We ordered one thinking we’d share something reasonable, and it was basically the size of a meal. No regrets. It was a nice reminder that even in the middle of learning, traveling, and working, it’s important to pause for a minute and enjoy where you are. Trips like this are important to us. Not just for the knowledge, but for what it allows us to bring back to the people we serve every day. And that’s always the goal! If you need a fresh start, we would love to be a part of it!

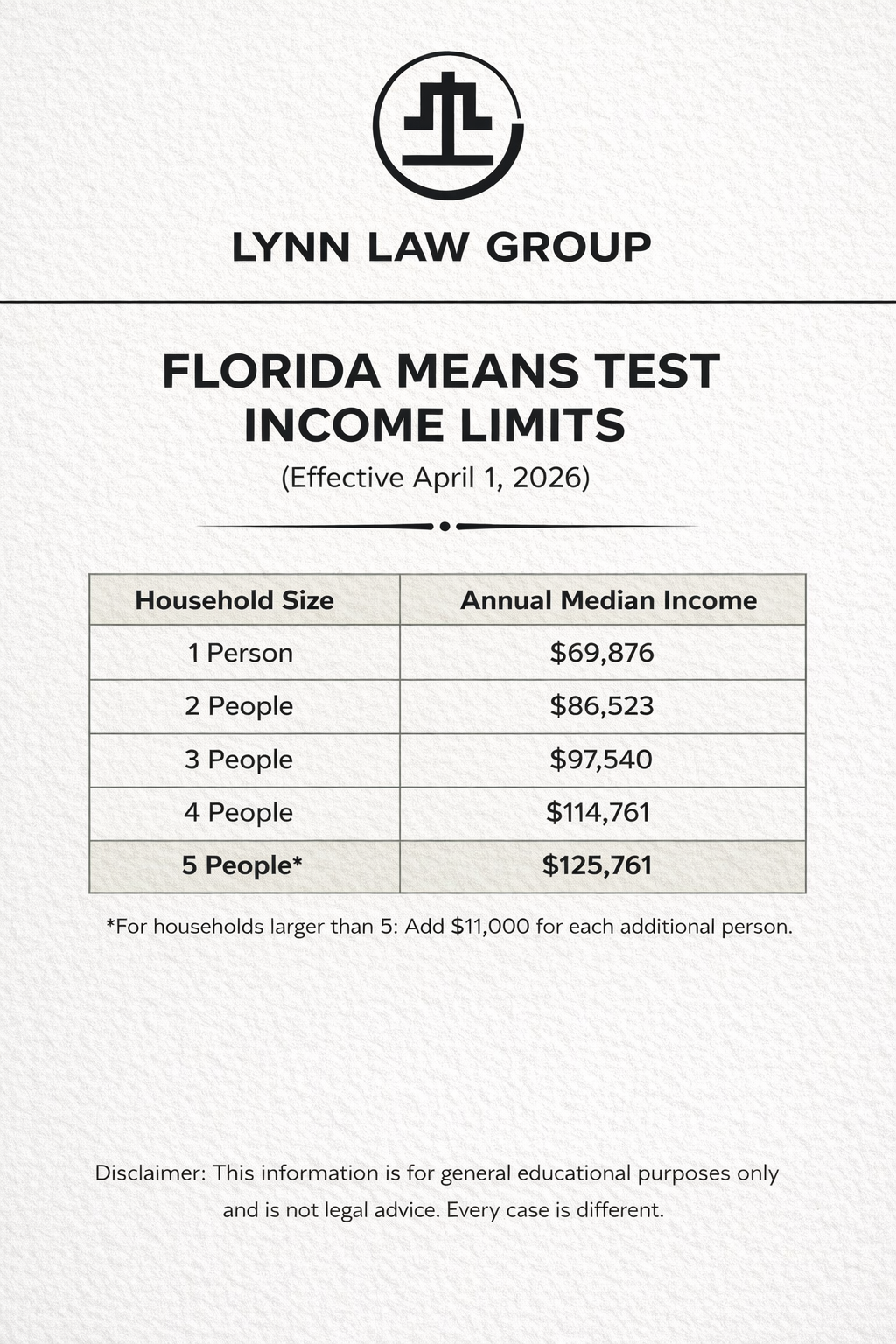

Florida's bankruptcy means test income limits updated April 1, 2026. See the new Chapter 7 income thresholds by household size, learn what changed, and find out if you qualify for debt relief.

Bankruptcy cases don’t pause for spring break. A Fort Myers bankruptcy attorney explains 341 meetings, timing strategy, and what Florida filers need to know right now.

Many people try debt settlement before considering bankruptcy — but it doesn’t always work as expected. Learn the risks, lawsuits that can follow, and when bankruptcy may provide stronger protection for people in Cape Coral and Southwest Florida.

Our bankruptcy attorneys attended the Paskay Seminar to stay current on developments affecting cases in the Middle District of Florida, including Fort Myers, Cape Coral, and Naples.

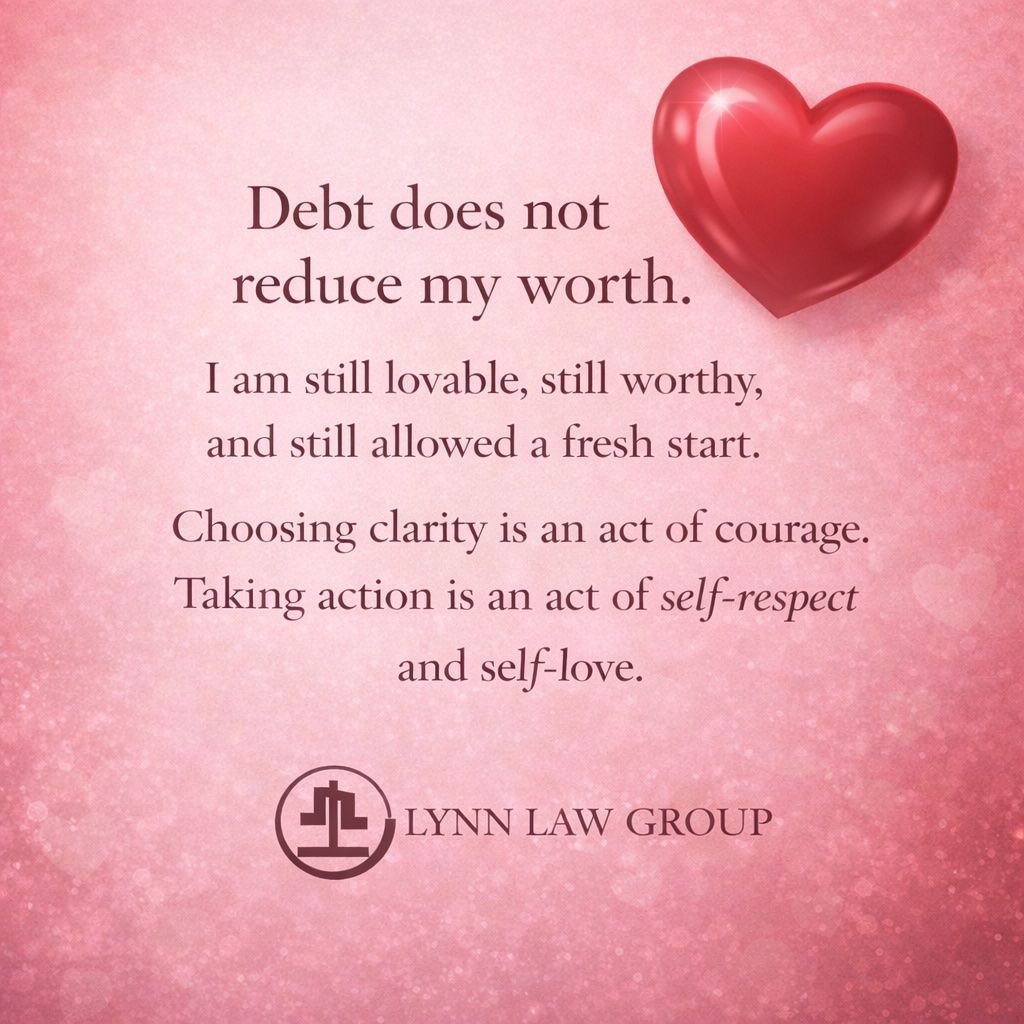

Valentine’s Day usually focuses on love: relationships, family, connection. But sitting where I sit every day, I see another side of it too. I see people who feel embarrassed to talk about money. People who apologize before they even sit down in my office. People who assume that needing help with debt says something negative about who they are. It doesn’t. Debt is a financial circumstance, a financial condition. It is not a reflection of character, intelligence, or worth. The Quiet Weight People Carry One of the hardest parts of financial stress isn’t always the numbers. It really is the shame that comes with it. I’ve met hardworking professionals, business owners, parents, retirees, and people who did everything “right” but still found themselves overwhelmed. Job loss, medical issues, rising costs, divorce, unexpected emergencies... life has a way of changing the math quickly. Sometimes it is just one life circumstance stacked on top of another one. And yet many people walk in believing they failed personally. They haven’t. Needing a solution doesn’t make someone less responsible. Often, it means they’re finally choosing to face things directly. A Fresh Start Is Not Giving Up There’s a common misconception that bankruptcy is about failure or losing control. In reality, I see the opposite. When someone chooses to learn their options, ask questions, and make a plan, that is an act of strength. It’s choosing clarity over fear. It’s deciding that protecting your family, your peace of mind, or your future matters more than continuing to struggle silently. For many people, the legal protections available through bankruptcy are simply tools... tools that exist so people can reset and move forward. Why This Message Matters The affirmation we shared recently says: Debt does not reduce my worth. I am still lovable, still worthy, and still allowed a fresh start. Choosing clarity is an act of courage. Taking action is an act of self-love. That isn’t just a nice sentiment. It reflects what I see every week in practice. Heck, what I saw today on Valentine's Day in the office. The moment clients understand their options, the shame starts to lift. You can almost see the weight come off their shoulders. Because information creates relief. And relief creates forward movement. If You’re Feeling Stuck If you’re reading this and feeling overwhelmed, here’s what I want you to know: You don’t need to have everything figured out before you ask questions. You don’t have to wait until things become an emergency. And your worth is never measured by your balance sheet. A fresh start isn’t about erasing the past... it’s about building a future that feels manageable again. ❤️ From all of us at Lynn Law Group, we hope this reminder reaches anyone who needs to hear it: financial challenges do not change your value.

Charged Off Debt in Florida: What It Really Means (And Why You Can Still Be Sued) If you’ve checked your credit report and seen the words “charged off,” you might have thought: “Okay, good. It’s gone.” I hear that assumption all the time in my Fort Myers office. But a charge-off does not mean the debt disappeared. It does not mean forgiveness. It does not mean cancellation. And it absolutely does not mean you can’t be sued. Let’s break down what it really means ... especially here in Southwest Florida. What Does “Charged Off” Actually Mean? When a credit card company marks an account as “charged off,” they are making an accounting decision, not a legal one. Typically, this happens after about six months of missed payments. The lender moves the account into a loss category on their internal books for tax and reporting purposes. That’s it. The debt still exists. You still legally owe it. A charge-off simply reflects how the creditor is treating the debt on their balance sheet. Does Charged Off Mean You Don’t Owe the Debt? No. This is one of the most common and most expensive misunderstandings I see. In fact, many collection actions happen after a debt is charged off. Once it’s written off internally, the original creditor may: Send the account to collections Sell it to a debt buyer File a lawsuit Seek a judgment Pursue wage garnishment after Florida judgment (if legally allowed) In Florida, once a creditor obtains a judgment, they can attempt garnishment, bank levies, or other collection remedies depending on your circumstances. So ignoring a charged-off account because you think it’s “gone” can lead to much bigger problems later. Why Lawsuits Often Happen After a Charge-Off Here’s what people don’t realize. After a charge-off, the original credit card company may sell the debt to a third-party debt buyer for pennies on the dollar. That debt buyer’s entire business model is collecting and that is often through lawsuits. We regularly see collection cases filed in: Lee County Collier County Charlotte County Throughout the Middle District of Florida Many people are shocked when they’re served with a lawsuit over an account they believed had already “disappeared.” It didn’t disappear. It changed hands. How Long Can a Creditor Sue You in Florida? Florida has a statute of limitations for credit card debt, but that doesn’t mean a debt becomes unenforceable immediately after charge-off. The clock usually begins running from the date of default, not the charge-off date, and there are nuances depending on the type of contract and the specific facts. This is why timing matters. If you’re unsure whether a debt is still legally collectible, don’t assume. Get clarity. What If the Debt Is Already on Your Credit Report as Charged Off? A charged-off account can remain on your credit report for up to seven years from the date of first delinquency. During that time, it can: Lower your credit score Be sold to multiple debt buyers Trigger collection calls Result in litigation Again, “charged off” is not the same as “resolved.” What Are Your Options in Florida? If you’re dealing with charged-off credit card debt in Fort Myers, Cape Coral, Naples, Lehigh Acres, Bonita Springs, or anywhere in Southwest Florida, your options may include: Negotiating a settlement Defending a collection lawsuit Asserting exemption protections Filing Chapter 7 bankruptcy Filing Chapter 13 bankruptcy Strategic timing to protect assets Every situation is different. Income, assets, home equity, vehicle equity, and prior judgments all matter. This is not something you want to guess about. The Bottom Line: Charged Off Does Not Mean Gone A charge-off is an accounting term. It is not forgiveness. It is not legal cancellation. It is not protection from a lawsuit. If you are overwhelmed by credit card debt, collection notices, or lawsuits in Florida, getting informed early is far less stressful than reacting after a judgment is entered. Work With a Florida Bankruptcy and Debt Attorney I’m Veronica Batt, a bankruptcy and debt attorney based in Fort Myers, Florida. At Lynn Law Group, we help individuals and families throughout: Fort Myers Cape Coral Naples Lehigh Acres Bonita Springs Estero Tampa Orlando Jacksonville throughout the Middle District of Florida All of Florida remotely If you’ve been told your debt is “charged off” and you’re unsure what that means for you, it’s better to ask questions now than deal with a garnishment later. This article is for informational purposes only. It is not legal advice and does not create an attorney-client relationship, you need to discuss your particular situation with a bankruptcy attorney.

Last week, members of the Southwest Florida bankruptcy community gathered to watch the 2026 State of the District Address delivered by the Chief Judge of the United States Bankruptcy Court for the Middle District of Florida. Although the address was presented remotely, our local professionals still came together in person. The Southwest Florida Bankruptcy Professionals Association (SWFBPA) hosted a watch party so attorneys, paralegals, trustees, and financial professionals across our region could hear the updates collectively and discuss what they mean for the people we serve here in Southwest Florida. I’m especially honored this year to be serving as the 2026 Vice President of the Southwest Florida Bankruptcy Professionals Association, an organization dedicated to improving communication, collaboration, and education within the bankruptcy system throughout our local district. A Noticeable Shift: Filings Are Increasing Again One of the realities discussed, and something many of us are seeing firsthand, is that bankruptcy filings have been gradually increasing year over year again That trend isn’t surprising. Families across Florida have been navigating: Higher insurance costs Increased interest rates Rising everyday expenses Fluctuating income in industries tied to housing and tourism In areas like Fort Myers, Cape Coral, Naples, and Bonita Springs, and Estero, these shifts are often felt quickly at the household level. When filings begin to rise, it’s usually not because people suddenly became irresponsible. More often, it’s because the financial margin that once existed has disappeared. For professionals working in this space, that trend is an important reminder: access to accurate information and steady guidance matters more than ever. Why Events Like the State of the District Matter The State of the District Address offers insight into: Current filing trends across the Middle District of Florida Operational updates from the court Emerging issues affecting debtors and creditors Practical realities professionals are seeing across the state Staying informed helps those of us who work directly with individuals and small business owners respond thoughtfully rather than reactively . When the system is functioning well...and when professionals are communicating...it becomes easier for people to stabilize their situation instead of spiraling further into crisis. Offering More Than Legal Answers As filings increase, I’m reminded that the most important thing many people need at the beginning isn’t a legal strategy, it’s simply someone willing to listen, without judgment. By the time most individuals reach out to a bankruptcy professional, they’ve often spent months or even years trying to hold everything together on their own. Many carry a significant amount of stress and, unfortunately, a lot of shame. One of the reasons I’m passionate about this area of law is that bankruptcy exists to provide a lawful, structured path forward. It was designed to give people: Protection Time to regroup Breathing room And ultimately, a genuine fresh start Helping clients understand that this process is a tool (not a personal failure!) is just as important as the legal work itself to me. Especially in times when filings are rising, it becomes even more important for professionals to offer not just technical knowledge, but also patience, clarity, and reassurance, they do call us counselors at law, after all! The Role of the Local Bankruptcy Community One of the most meaningful parts of the SWFBPA watch party was seeing so many different professionals in one room. All people who all play a role in helping the system function fairly. Bankruptcy is never handled by a single person. It requires coordination between: Judges Trustees Attorneys Court staff Financial professionals When those groups stay connected, the process tends to work more smoothly for the individuals at the center of it, the families trying to regain stability. SWFBPA’s mission has always been to strengthen that collaboration here in Southwest Florida, and events like this reinforce why that effort matters. Flipping the Script on the Conversation Around Debt Even as filings rise, many people still hesitate to ask questions because of the stigma surrounding bankruptcy. In reality, most financial hardship is tied to life events or economic shifts, not personal character. Normalizing conversations about debt allows people to: Seek help earlier Avoid unnecessary escalation Preserve more of what they’ve worked hard to build For many Florida families, simply having a safe place to ask questions without judgment is the first step toward real financial recovery. Moving Forward with Purpose Serving as Vice President of SWFBPA this year has reinforced something I see every day: when professionals stay informed, collaborative, and focused on practical solutions, the bankruptcy system works the way it was intended. The goal is never to push someone toward filing. The goal is to make sure that if relief is needed, people understand their rights and their options...and can move forward with clarity and dignity instead of fear. As economic pressure and distress continue to affect households across Fort Myers, Naples, Cape Coral, Bonita Springs, and the surrounding Southwest Florida communities, offering clients a listening ear, steady guidance, and reliable knowledge is more important than ever. For many, that combination is what finally makes a fresh start feel possible. About the Author Veronica Batt is a bankruptcy attorney based in Southwest Florida, serving all of Florida, and currently serves as the 2026 Vice President of the Southwest Florida Bankruptcy Professionals Association. Her work focuses on helping individuals and families understand their financial options, reduce fear and shame around the process, and move toward long-term stability with dignity.